The old mental model of an insurance claim is too human. A lawyer sends a demand. An adjuster reads the file. The two sides negotiate.

That still happens. But the file may now be shaped before the adjuster ever gets to judgment. A claim can be triaged, summarized, scored, benchmarked, routed, and flagged by software. The demand package can be condensed by AI. Medical bills can be reviewed against pricing databases. Treatment gaps, prior injuries, inconsistent statements, provider patterns, and fraud indicators can be surfaced automatically.

The strategic question for personal injury firms is not whether insurers use AI. They do. The better question is whether the firm has a counter-system: a way to make the file cleaner, earlier, more structured, more verifiable, and harder to undervalue.

This is where insurance AI claims personal injurystrategy becomes an operating issue. Firms do not counter carrier analytics by buying a random AI tool. They counter it by building firm-owned workflows around intake, records, medical specials, demand preparation, negotiation intelligence, and vendor governance.

In plain English

Insurance companies use AI and machine learning to process claims faster, spot patterns, flag risk, benchmark bills, and guide settlement decisions. That does not mean a robot decides every claim, but it does mean the file is increasingly filtered through data systems before and during negotiation. PI firms should respond by building their own structured workflows: clean case data, early weakness detection, machine-readable demands, human review gates, and negotiation intelligence.

What insurer AI is actually doing

The National Association of Insurance Commissioners says AI is used across the insurance life cycle, including claims handling and fraud detection. Its model bulletin also reminds insurers that AI-supported decisions must still comply with laws on unfair trade practices, unfair claims settlement practices, and unfair discrimination.

Public vendor materials show what that looks like in the casualty workflow. CCC describes third-party casualty tools for medical bill review, demand-package intake, general damages, pricing benchmarks, AI-powered medical-record synthesis, impact severity from vehicle photos, digital information capture, and settlement offers. Verisk describes bodily-injury decision tools that use predictive medical and settlement models, summarize demand packages, highlight medical and valuation considerations, detect provider alerts, apply liability modules, and connect with ClaimSearch. Guidewire describes predictive analytics for P&C insurers covering claims triage, settlement, litigation detection, and auto bodily-injury outcomes.

None of that is science fiction. It is the operating stack on the other side of the negotiation table.

The clean way to think about it: insurer AI helps carriers decide which files need attention, what the file appears to be worth, where the weaknesses are, what needs investigation, and how quickly the claim can be resolved.

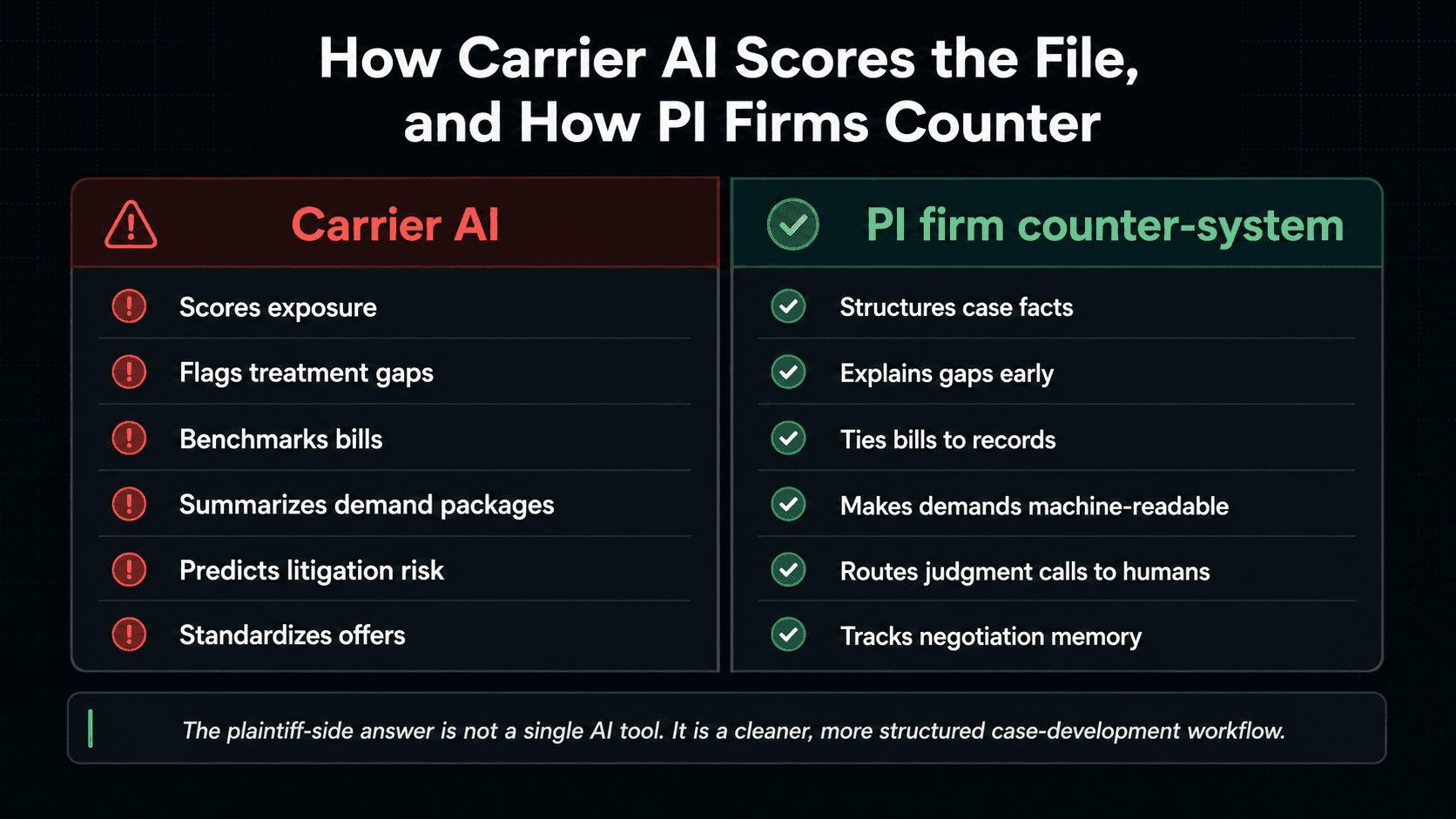

The insurer AI playbook, and the PI counter-system

PI firms should not mirror the carrier blindly. The plaintiff-side job is different. The firm is not trying to minimize payout. It is trying to build a complete, credible, well-supported case while protecting client data and preserving attorney judgment.

| Carrier workflow | How insurers use AI | PI firm counter-system |

|---|---|---|

| Claims triage | Predictive models score which claims look complex, expensive, likely to litigate, or likely to involve an attorney. | Build a front-loaded case classification workflow that identifies liability, injury severity, treatment status, venue, coverage, and risk signals before the carrier frames the file. |

| Medical bill review | Bill-review platforms benchmark charges, flag anomalies, validate paid amounts, and standardize recommendations. | Maintain a medical-specials layer that ties bills to records, CPT or diagnosis context where available, treatment chronology, causation support, and known gaps. |

| Demand-package synthesis | AI tools summarize demand packages, surface key medical facts, and help adjusters review high-volume records faster. | Write demands for both humans and machines: structured chronology, exhibit map, gap explanations, uncertainty notes, and a clear damages table. |

| Fraud and anomaly detection | Carriers use text, image, audio, video, social, provider, and network data to flag suspicious patterns or inconsistent details. | Run an internal contradiction check before demand: statements, records, bills, social risk, prior injuries, provider patterns, and missing documentation. |

| Impact and damage analysis | Computer vision and vehicle-photo analysis can estimate damage, infer impact severity, and inform bodily-injury exposure decisions. | Preserve photos, repair estimates, crash data, medical onset, mechanism of injury, and expert review paths where low visible damage does not match real injury. |

| Settlement guidance | Settlement and liability tools benchmark claims against historical outcomes, venue patterns, company payment trends, and adjuster workflows. | Track carrier, adjuster, venue, injury, treatment, offer, demand, litigation, and outcome data so negotiation posture is evidence-based, not anecdotal. |

Why this changes the economics of claims work

In a manual world, carriers had an advantage because they had more staff, more claims history, and more repeatable process. In an AI world, that advantage compounds. The carrier can process more files, spot more patterns, route claims faster, and standardize settlement posture across thousands of matters.

The risk for PI firms is not that AI makes every carrier right. The risk is that a messy file becomes cheaper to discount. If treatment gaps are unexplained, if prior injuries are not distinguished, if bills are disconnected from the records, if the client's statements vary across forms, if liability facts are buried, or if the demand is a narrative with no structure, the carrier's systems have more room to frame the claim against the client.

That is why the plaintiff-side answer is not only better demand writing. It is better case development upstream of the demand.

Seven workflows PI firms should build now

1. Build a claim intelligence layer

Every case needs a structured timeline of liability facts, symptoms, treatment, diagnostics, bills, wage loss, client communications, offers, and missing evidence. The point is not prettier notes. The point is a source of truth the firm can use before the carrier reduces the case to a score.

2. Map the insurer's likely scoring triggers

PI firms should assume the file will be evaluated for delayed treatment, treatment gaps, prior injuries, inconsistent statements, low property damage, provider anomalies, billing benchmarks, social-media contradictions, and attorney or venue history. The counter is not hiding weaknesses. It is identifying, explaining, documenting, or escalating them early.

3. Make the demand package machine-readable

A demand should be easy for an adjuster, a supervisor, and an AI summary layer to understand. Use clear headings, a chronology, exhibit labels, cited records, a specials table, gap explanations, prior-injury distinctions, liability facts, and a concise theory of damages.

4. Use AI for internal contradiction review

Before sending the package, run a review that asks: What will the carrier attack? What facts appear inconsistent? Which records are missing? Which symptoms are unsupported? Which bills look disconnected from treatment? Which questions require attorney review?

5. Create escalation rules for judgment calls

AI can flag a treatment gap, prior injury, questionable causation note, lien issue, or possible social-media risk. It should not decide case value, legal strategy, client advice, or settlement authority. Those issues need explicit human-review gates.

6. Track negotiation intelligence

Carrier AI learns from carrier history. PI firms need their own memory: initial offers, adjuster behavior, delay patterns, venue outcomes, provider reductions, litigation triggers, and settlement deltas. Without this, each negotiation starts from staff memory instead of institutional evidence.

7. Govern the tools and vendors

The firm should know which AI tools touch client data, where that data goes, whether outputs are logged, what gets reviewed by humans, and which vendor systems may train on or retain sensitive information. Vendor risk is part of claims strategy now.

The demand package has to be built for humans and machines

PI lawyers often think of the demand package as persuasion. It is. But it is also data architecture.

A carrier-side AI summary layer will not admire a beautiful paragraph if the facts are hard to extract. It will look for dates, diagnoses, treatment, charges, gaps, prior conditions, liability signals, inconsistencies, and documents. If those are scattered, the machine summary may miss the point before the human negotiator ever reads the nuance.

The counter is a demand package that is emotionally persuasive and operationally legible:

- One clear liability theory.

- A treatment chronology with record cites.

- A medical-specials table tied to provider records and bills.

- Explicit explanations for treatment gaps or delayed care.

- Separate sections for prior injuries, aggravation, and causation support.

- A map of exhibits and what each exhibit proves.

- Human-reviewed notes on uncertainty and disputed facts.

This is not about writing for a machine instead of a person. It is about making the person and the machine see the strongest version of the same file.

Fraud detection is a workflow risk, not just a client risk

Insurers are investing heavily in fraud and anomaly detection. Deloitte describes AI use cases across text analytics, social-media analysis, audio-image-video analysis, photo metadata, telematics, geospatial data, and simulation models for provider and repair-shop patterns. The NAIC Journal of Insurance Regulation notes that insurers use or are considering AI/ML to identify claims for further investigation, detect first- and third-party liability, identify medical-provider fraud, and analyze social media in some lines.

A good PI firm should not treat this as a reason to become defensive or vague. It should treat it as a reason to run its own quality control earlier.

Before demand, the firm should know whether there are unexplained gaps, conflicting statements, missing records, confusing prior injuries, questionable billing patterns, or social posts that may be misunderstood. Some items will be harmless. Some will need context. Some will require attorney judgment. The point is to find them before the carrier's system does.

The governance lesson cuts both ways

Regulators are increasingly focused on insurer AI governance. The NAIC model bulletin says AI-supported consumer-impacting decisions must comply with insurance laws and that regulators may request documentation about an insurer's AI systems. California's insurance bulletin on bias and unfair discrimination says insurers must conduct due diligence before using fraud algorithms or claims tools and that the Department reserves the right to audit claims criteria, programs, and practices.

PI firms should absorb the same lesson for their own side. If the firm uses AI on client files, it needs rules: approved tools, data boundaries, human review, escalation paths, audit logs, vendor review, and clear prohibitions on unsupervised legal advice. This is why AI governance and vendor-risk controls are not back-office details. They are part of claims strategy.

Where to start

Do not start by trying to automate every claim. Start with the bottleneck most exposed to carrier scoring.

For many PI firms, the first useful system is records chasing and case development. Missing records, bills, imaging, authorizations, and provider responses create weaknesses the carrier can use. For firms with heavy lead spend, the starting point may be AI intake automation or after-hours intake workflows, because case quality is shaped from the first call. For firms with high client-call volume, it may be client communication systems that keep facts current and prevent avoidable dissatisfaction.

The mature answer is a portfolio of AI systems for personal injury firms, built one workflow at a time. The goal is not to out-hype the carrier. The goal is to make the firm's operating model harder to exploit.

This is also the deeper point behind our pieces on tools versus systems and moving from prompts to systems. Better AI use is not a prompt library. It is a repeatable operating system.

Sources and research notes

This article draws on public regulator materials and insurance-vendor materials, including the NAIC model bulletin on AI systems by insurers, the NAIC's insurance AI topic page, the NAIC Journal of Insurance Regulation article on AI and insurance regulation, CCC's public materials on third-party casualty claims, Verisk's Liability Navigator materials, Guidewire's public pages on predictive analytics and Claims Intel, Deloitte's discussion of AI in insurance fraud detection, and California Department of Insurance guidance on bias and unfair discrimination in claims practices.

Health-insurance litigation over algorithmic claim decisions, such as reporting on Cigna's PxDx process and litigation involving UnitedHealth's disputed nH Predict allegations, is not the same as a third-party auto bodily-injury claim. It is still relevant as a warning: courts and regulators are increasingly interested in how algorithmic claim systems work, who reviews them, and whether human judgment is real or symbolic.

Frequently asked questions

How are insurance companies using AI in personal injury claims?

Insurers use AI and predictive analytics for claims triage, medical bill review, demand-package synthesis, fraud detection, injury evaluation, impact analysis, liability review, settlement guidance, and litigation-risk prediction.

Does insurance AI automatically deny personal injury claims?

Not usually. In liability and casualty claims, AI more often supports adjusters by scoring, summarizing, routing, benchmarking, or flagging claims. That still matters because those scores and summaries can shape how the file is handled.

What claim facts do insurer AI systems look for?

Common signals include treatment gaps, delayed care, prior injuries, inconsistent statements, low visible vehicle damage, provider billing anomalies, medical-record contradictions, fraud indicators, attorney involvement, venue, and litigation risk.

How can PI firms counter insurer AI?

PI firms should build a counter-system: structured case data, early gap detection, machine-readable demand packages, internal contradiction review, human escalation rules, negotiation intelligence, and vendor-risk governance.

Should personal injury firms use AI for medical record review?

Yes, if it is scoped carefully. AI can summarize records, build timelines, identify missing documents, and flag uncertainty, but case managers and attorneys should review important medical, causation, and legal conclusions.

Can AI help with demand letters?

AI can help organize chronology, exhibits, treatment summaries, specials tables, and issue spotting. It should not replace attorney judgment on case value, legal theory, settlement authority, or sensitive client advice.

Why does vendor risk matter in claims AI?

Claims AI often touches medical records, client facts, liens, settlement data, and strategy. Firms need controls for confidentiality, retention, training use, access, audit logs, human review, and whether the system is firm-owned or vendor-owned.

The firms that adapt will not be the ones that merely tell staff to use AI. They will be the ones that use AI to make case facts cleaner, weaknesses visible earlier, demands more structured, and negotiation memory more institutional.

Insurer AI is an operating system. The answer is a better operating system on the plaintiff side.

Find the workflow carriers can exploit

Possible Minds starts with a diagnostic: where the file leaks value, which workflow is ready for AI, and what controls need to exist before automation touches client data.

Book a Diagnostic Call